Top Stories of the Week - 4/5

This week in the newsletter, we write about discussions about changing Ethereum’s issuance schedule, the forthcoming launch of a new Bitcoin token protocol, and the ruckus being created in DeFi by Ethena.

Subscribe here and receive Galaxy's Weekly Top Stories, and more, directly to your inbox.

Maker Ethena Integration Raises Red Flags

MakerDAO is moving forward with plans to allow up to $1 billion of DAI, Maker’s overcollateralized stablecoin, to be borrowed against Ethena’s USDe and sUSDe collateral. The new proposal comes less than a week after an initial proposal passed allocating $100 million for the same vault. Ethena is a newly launched cash and carry product that returns yield to its token holders. Demand for leverage has led to yields ranging from 20%-120% APY, resulting in a a flood of capital moving to the application. It has amassed nearly $2 billion in TVL in under 6 months.

On March 29, Maker launched a vault for holders of USDe and sUSDe to borrow DAI. The vault was launched using a new decentralized lending protocol called Morpho. Maker uses a mechanism called the Direct Deposit Module (D3M) to facilitate borrows on Morpho. The D3M enables the Morpho vault to mint DAI directly and lend it against an overcollateralized position. The vault filled up within hours after launching and on April 1 a new proposal was put forward suggesting an additional $600 million DAI be made available to borrow with the possibility to eventually increase the total amount to $1 billion.

The announcement was met with mixed results. Aavechan founder Marc Zeller almost immediately submitted a proposal to remove Maker’s D3M deployment from Aave, citing Maker’s decision to increase Ethena exposure as being too risky. Alternatively, Maker’s founder Rune and MakerDAO members that drafted the proposal were enthusiastic, outlining the deployment of additional DAI as a huge revenue opportunity with manageable risk.

At the time of writing, the new proposal has been approved by Maker governance to proceed to an executive vote which will likely occur the week of April 8. Separately, MakerDAO also has another proposal under consideration to enable a centralized arranger to facilitate a similar trade on behalf of Maker. That proposal will likely move to an initial vote in the coming month.

OUR TAKE:

Concerns over Maker’s risk management are largely a result of two issues: (1) Maker’s ongoing transition to Endgame and (2) a lack of agreement over Ethena’s risks.

Endgame is a multi-year plan to revitalize Maker governance and grow DAI usage. It is complex and includes significant alterations to Maker’s existing form through the introduction of subDAOs – smaller organizations that borrow DAI from Maker to generate returns - and the creation of specialized AI models for governance.

Maker’s transition to Endgame has been bumpy, as is to be expected and governance participation has declined. Last month, Maker suddenly announced an increase in rates, raising some initial concerns about the lack of messaging ahead of time. The sudden movement toward Ethena integration last week reignited those concerns and led to a perception that MakerDAO governance remains opaque and controlled by Rune. Maker delegate PaperImperium has been especially vocal, highlighting the lack of traditional risk analyses or time elapsed that would traditionally accompany this type of deployment.

These concerns have been exacerbated by an ongoing debate in the crypto industry over Ethena’s risks. This was the primary issue raised by Zeller, who argued that Maker’s Ethena integration made the risk/reward of integrating DAI no longer worth it. There are likely also some competitive dynamics at play as Zeller’s proposal would incentivize more use of GHO. Aave’s own stablecoin. There are clearly risks to Ethena, but a number of Maker contributors and outside observers have since released more in-depth analysis to help individuals understand and determine for themselves the full extent of it.

The last week of controversy was largely brought upon Maker by itself. There are legitimate reasons for Maker to pursue an integration with Ethena, but it is the responsibility of Maker governance to ensure that everyone understands those reasons and why they outweigh the risks. Greater governance transparency and engagement is at the heart of Endgame’s creation. Failure to deliver so far can be partially attributed to Maker being in a transition period. With the launch of the first SubDAO later this year, however, the pressure is on to demonstrate Maker’s new governance is yielding results. - Lucas Tchyan

New Fungible Tokens Coming to Bitcoin Soon

Runes is a new fungible token protocol on Bitcoin that is set to launch on the halving block (block 840,000) on April 20, 2024. The creator of Runes, Casey Rodarmor, who also created Ordinals, released the official documentation for the Runes protocol this week after proposing Runes back in September 2023.

Runes is a UTXO-based fungible token standard that leverages the OP_RETURN field in Bitcoin transactions. This field permits the inclusion of arbitrary data, such as text or image data, up to 80 bytes within a Bitcoin transaction. The Runes protocol enhances data storage efficiency by utilizing the OP_RETURN field to store token data, a method that is more efficient than storing data in the witness field like BRC-20s. The token metadata stored in the OP_RETURN field includes details such as the token name, divisibility, minting information, and symbol. The process of inputting this data into the OP_RETURN field is known as "Etching" and becomes immutable once the Etching is completed.

The unspent transaction output (UTXO) based approach for Runes entails that the balance of a Runes collection is contained directly in the UTXO set. UTXOs containing Runes are then split into several new UTXOs when users purchase or mint the Runes token. For reference, the unspent transaction output (UTXO) accounting model is how every Bitcoin transaction is recorded on-chain. By taking a UTXO based approach, Runes token transfers are no different than standard Bitcoin transactions.

The user experience of purchasing, selling and minting Runes will be identical to Ordinals/BRCs. However, the transactions for Runes tokens take up significantly less blockspace. Below is a table highlighting the differences between Runes and BRC-20s.

OUR TAKE:

Runes is a potential solution to the inefficiencies that exist with BRC-20s, the largest fungible token standard on Bitcoin today. BRC-20 related transactions bloat Bitcoin's blockspace by requiring two on-chain transactions to mint or transfer tokens. As a result, BRC-20s create unnecessary extra UTXOs. Given that BRC-20 related inscriptions constitute more than 90% of all inscriptions, the requirement for two on-chain transactions per BRC-20 token mint or transfer has created significant challenges related to fee spikes.

While fee spikes are not inherently bad for the Bitcoin network and are good for miners, fee spikes due to an asset’s egregious technical inefficiencies is not sustainable. Runes is a promising alternative to BRC-20s as the minting or transferring of Runes tokens requires one on-chain transaction. The Runes token standard is able to achieve this through its UTXO based design that utilizes the OP_RETURN field instead of the segregated witness field. According to Casey Rodarmor, "UTXO-based protocols fit more naturally into Bitcoin. It minimizes the production by avoiding the creation of garbage UTXOs."

Runes are also generating high anticipation due to its planned launch on the halving block (block 840,000). The association of Runes and the halving is driving additional interest for Runes as all transactions in the first halving block will hold historical significance solely from being included in that block. Collectors are already positioning themselves to receive Runes airdrops though purchasing Runes associated Ordinal collections like Runestones and RSICs, which have seen a combined $179.4m in trading volume. Holders of Runestones and RSICs are expected to receive airdrops from the first batch of Runes collections. (Notably, the market has no concrete information on the details of the first set of Runes collections.)

The 52m transactions and 4.8k BTC paid in fees for BRC-20s in the past year is a clear signal that there is demand for fungible tokens on Bitcoin. Although BRC-20s are extremely inefficient, the broader market invested heavily in BRC-20s like ORDI, which now trades at a $1.3bn fully diluted valuation. The rapid success of BRC-20s is nothing to gloss over—BRC-20s are listed on major exchanges like Binance through spot and perceptual futures markets. But Runes holds a significant advantage by launching after BRC-20s, as the trading infrastructure for fungible tokens on Bitcoin is already established. Despite BRC-20s having a first-mover advantage, there is potential for the invested capital in BRC-20s to rotate into Runes. Notably, Casey Rodarmor stated, "Runes were built for degens and memecoins, but the protocol is simple, efficient, and secure." Given the current market trend surrounding memecoins, the timing of the Runes launch is particularly favorable. - Gabe Parker

Controversy Grows Over Proposal to Change Ethereum’s Issuance Policies

Prominent Ethereum community members are pushing back against a proposal to decrease the ETH issuance rate. The proposal, created by Ethereum Foundation Researchers Ansgar Dietrichs and Caspar Schwarz-Schilling, recommends a new issuance schedule that, at current staking levels, would reduce staking rewards by roughly 30% for validators. The long-term goal of the proposal is to achieve a target range of staking ratios, that is percentage range of total ETH supply staked, thereby limiting the economic value that can accrue to liquid staking providers such as Lido. Since the creation of the proposal on February 21, Dietrichs and Schilling have sought feedback from the community on their ideas by presenting the proposal on All Core Developer calls, as well as crypto podcasts such as Uncommon Core, and engaging in discussions with the community about this topic on various social media platforms like X, Discord, and Farcaster.

This week, the conversation about changes to issuance sparked opposition from several prominent community members including Gnosis co-founder Martin Köppelmann, EIP 1559 co-author Eric Conner, Coinbase Protocol Specialist Viktor Bunin, Dba co-founder Jon Charbonneau, Ethereum ecosystem angel investors Mariano Conti and “DCinvestor”, among others. Many pointed out that a reduction in issuance may not materially reduce the staking rate of Ethereum or positively impact stake distribution away from liquid staking providers. The general sentiment among people who opposed the proposal was to conduct further research on what the minimal viable issuance schedule of Ethereum should be long-term and consider policies that may have a more direct impact on the adoption of liquid staking solutions. Further, some community members pointed out that changes to issuance would be especially unwise during a time when the U.S. Securities Exchange Commission (SEC) is actively investigating Ethereum and potentially building a case to classify ETH as a security.

OUR TAKE:

It is unclear what the criteria are in the eyes of U.S. regulators for classifying cryptocurrencies as securities. However, based on the classification of bitcoin as a commodity, one of the criteria that is used to evaluate the classification of a cryptocurrency is its level of decentralization. The only cryptocurrency that the SEC has affirmed to be outside of the scope of its jurisdiction is Bitcoin and at least one of the arguments for why Bitcoin is a commodity, and not a security, is that there is no central entity or authority controlling the supply and demand for the asset. Therefore, changes to the supply of ETH may be an important factor in how regulators view the decentralization of Ethereum. However, if this is the case, then conversations about how to change the supply of ETH are unlikely to have any greater impact on regulators’ view of Ethereum decentralization than the multiple upgrades that have actually and radically changed the supply of ETH in recent years.

Ethereum upgrades necessarily require coordination, communication, and funding between various stakeholders in the ecosystem to execute successfully. They are also difficult to continue organizing as the ecosystem grows without some degree of centralization and spearheading efforts by a central entity, such as the Ethereum Foundation. Due to the network’s upgradeability, Ethereum is not as decentralized as Bitcoin. However, the important question is whether Ethereum is sufficiently decentralized in the eyes of U.S. regulators to be classified as a commodity like Bitcoin because while Ethereum may not be as decentralized as Bitcoin, it is more decentralized and harder to upgrade than other blockchains. In this way, decentralization is a spectrum and as a criterion for evaluating the classification of cryptocurrencies by the SEC difficult to define or measure. It is almost always understood in relative terms and pinpointing at what threshold a cryptocurrency may become a commodity in the U.S. continue to confound the crypto industry.

On the current proposal to change Ethereum’s issuance policies, it is clear that not even the authors of the proposal are confident about what precise changes should be made to issuance to achieve long-term minimal viable issuance of ETH or limit the growth of liquid staking providers. Dietrichs has repeatedly emphasized that the proposal is primarily meant to spark discussion and debate on the topic. They also agreed with the opposition to their proposal that there needs to be further research on the impacts of issuance changes on staking dynamics. Further, because any changes to issuance will impact a larger community of ETH holders than before the Merge upgrade (when issuance impacted only miners) any changes proposed by developers will likely be more difficult to rally support for and thus, take longer to implement. For these reasons, it is unlikely that any changes to issuance will end up being included in the next immediate Ethereum hard fork, Pectra. - Christine Kim

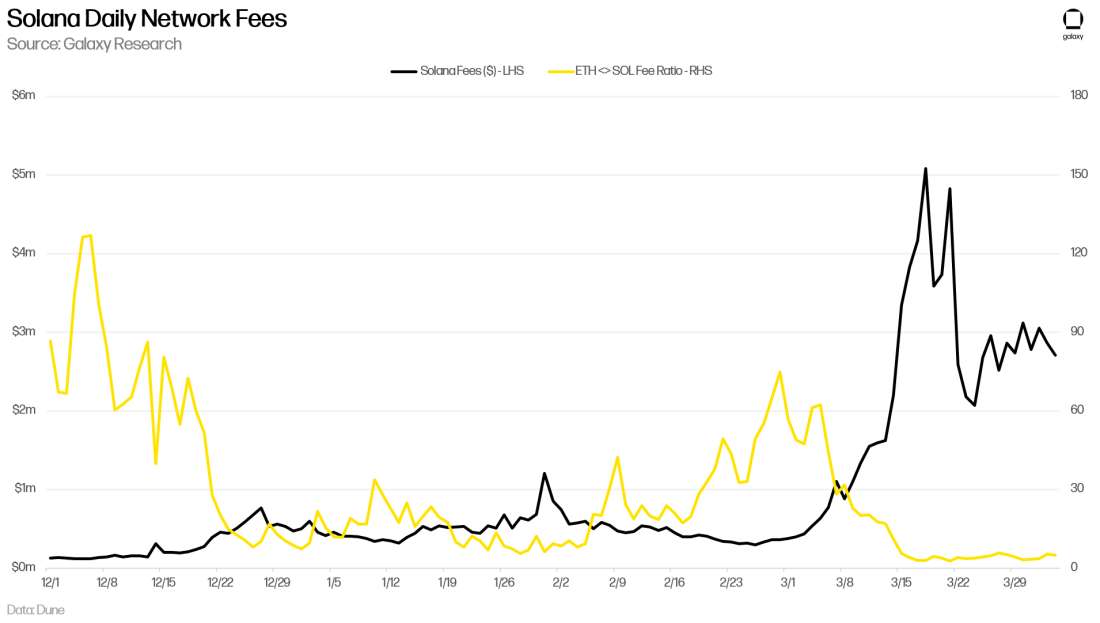

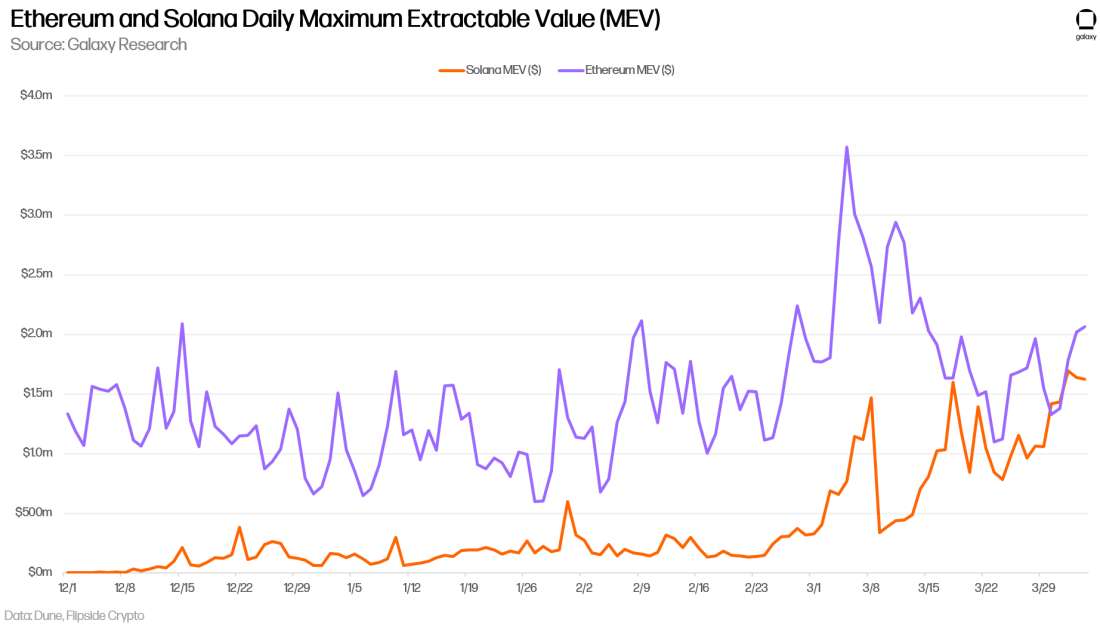

Charts of the Week

Daily fees on Solana made an all-time high of $5.08m on March 18, 2024 and have remained elevated above its three-month daily average of $1.17m for the last 31 days. The gap between fees generated by Solana and Ethereum, the highest fee revenue generating blockchain, has closed substantially over the last four months. The ratio of Ethereum daily fees to Solana daily fees reached its lowest point ever on March 21, 2024 at a ratio of 2.69 times. On this day the average transaction fee on Solana was $0.061 compared to Ethereum’s $11.90.

At the same time, the amount Maximum Extractable Value (MEV) on Solana cleared that of Ethereum for two consecutive days on March 30, 2024 and March 31, 2024. Over these two days Solana did nearly $2.9m in MEV compared to Ethereum’s $2.7m. MEV is indicative of the amount of economic activity on a given chain. Solana’s MEV rising above Ethereum’s is a signal that economic activity is reaching towards that of Ethereum’s.

Other News

Ethena Labs adds bitcoin as USDe backing asset

Binance set to end Bitcoin NFT support despite recent surge in interest

US PayPal customers will be able to use stablecoin for international payments

Galaxy Digital to launch $100 million fund for early-stage crypto companies

Wormhole to begin airdrop claims of over 670 million tokens

Tether's bitcoin holdings cross $5 billion mark after latest purchase

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2024. All rights reserved.