Backing Mesh to Connect Our Financial World

"Our country has always benefited when markets were more decentralized, when they're not dominated by a handful of incumbents... I want a financial market where consumers can switch products more seamlessly, and where financial companies have to constantly compete to keep them… Our goal is to accelerate the shift toward open banking and ultimately give more leverage to consumers to find the products best for them.”

-- Rohit Chopra, Director of the Consumer Financial Protection Bureau (“CFPB”) - link

THE NEW PARADIGM OF OPEN BANKING

The financial services market has been talking about “Open Banking” for the better part of the last decade. Open Banking—a concept and philosophy that consumers should own and be able to share their financial data to access innovative financial services—despite all its benefits, has felt more idealistic than reality. However, the CFPB’s new rule proposal in October was a watershed moment and one that is poised to “jumpstart competition and accelerate [the] shift to Open Banking.”

These rule changes are great for consumers of financial products in the United States, which has lagged other geographies across the world in terms of Open Banking adoption. They are likely to establish consumer protections around data, supercharge competition by reducing data moats held by incumbents, and reduce fees. They transfer control away from banks toward consumers who will have “more power to walk away from bad service and choose financial institutions that offer the best products and prices.”

Open Banking and the crypto community share many of the same principles—decentralization, customer empowerment, transparency, etc. Given this philosophical overlap, the crypto industry has been fertile grounds for entrepreneurial activity accelerating this shift.

REDESIGNING THE FINANCIAL USER EXPERIENCE

The average consumer has multiple financial accounts, creating fragmentation across many bank accounts, brokerage / retirement accounts, fintech/neobank applications, digital wallets, crypto exchanges, etc. Despite the innovation we’ve seen across fintech over the last decade, our financial lives are disintegrated and don’t offer connectivity across these services—something Open Banking and crypto are destined to help solve.

Imagine a world where your financial life is unified: where you can use funds sitting in your Robinhood account to fund a trade on Coinbase; where cash sitting idle in your Venmo wallet can be used to purchase goods on Amazon; where an enterprise or small business can use its assets cross-platform in the same manner.

This world would require a network that facilitates communication and secure & compliant asset transfers between isolated financial platforms. Moreover, it would require a magical user experience that allows users to “pull” assets seamlessly from one account to another.

THE MODERN “MESH” NETWORK

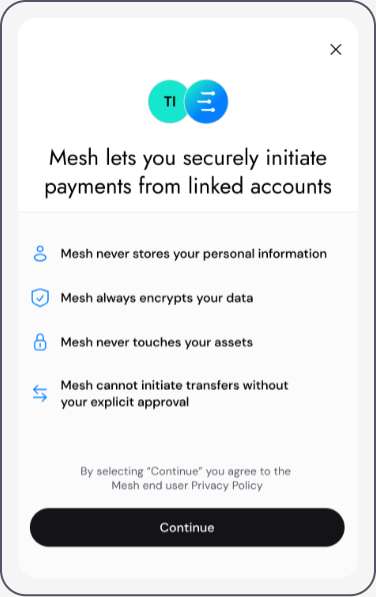

Our portfolio company, Mesh, enables this future world. Mesh is a financial ecosystem that enables users to seamlessly move assets (crypto, equities, etc.) between their disparate financial accounts and wallets, without ever leaving their native fintech application—think “Plaid but with the read, write, and transfer capabilities.” Mesh has more than 300 platform integrations across crypto and TradFi with a vision to build a seamlessly connected financial ecosystem that prioritizes openness, accessibility, and user-friendliness for both businesses and consumers.

Mesh establishes secure, scalable, and compliant API integrations with brokerages, financial institutions, crypto exchanges, and wallets, in order to build an open, connected, and secure financial ecosystem. Mesh’s infrastructure provides a magical product experience for users who want to move assets across a wide range of applications.

This integration engine is Mesh’s secret sauce and something the Mesh team was uniquely positioned to build. With deep experience across financial software, security, and compliance, Mesh was founded by Bam Azizi and a group of technologists from NoPassword (acquired by LastPass). The integrations and identity services built during their time at NoPassword are currently still used by major financial institutions.

Mesh’s value proposition for users is simple and it fulfills the promise of Open Banking by giving users more control. Mesh also provides a compelling proposition for fintech platforms, who are eager to improve conversion of funds onto their application in a compliant manner (see Travel Rules). The value propositions are strong and have led to impressive pull in the market across a number of use cases including:

Embedded Crypto Deposits: Enables companies to keep users in their app as they deposit crypto.

Crypto Payments: Enables users to make payments directly from their existing accounts on all major exchanges and wallets.

Seamless On-Ramping: Enables users to buy crypto using balances and payment methods in the KYC’d exchange accounts they already have.

THE FUTURE OF FINANCE

Today, Mesh announced their latest investment from PayPal Ventures. The investment will be made almost entirely in PayPal USD (PYUSD), PayPal’s U.S. dollar denominated stablecoin, and will be transferred on-chain using the Mesh API. This is a big moment for the company and one Galaxy is excited to be a part of.

Similar to how the internet has been moving from ”read” to “write” to “own”, our financial lives are undergoing the same paradigm shift. We are entering a new era where TradFi and crypto products are converging via Mesh, enabling users to write and own our assets with more autonomy and ease.

From neobanks and self-custody crypto wallets, to exchanges, DeFi, personal finance and investing, Mesh’s use cases hit every corner of finance. We can’t wait to see what the future looks like in a world where our assets are unified through Mesh.

*Mesh is a portfolio company of Galaxy’s Venture arm.

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2024. All rights reserved.