This is the first part of a 3-part series originally published in 2019. Read part 2, On Free Markets for Money, here. Read part 3, On Incentives & Scarcity, here.

Abstract

An essay on the hazards of unsound money, savings behavior under unsound monetary orders, the common fallacies of modern central banking, and the prospect of digital sound money.

Introduction

The choice of which money to use comes with tradeoffs and consequences. Money that is costly to create has generally served as the more reliable form of currency, since the ability to create money inexpensively destroys the wealth of savers and hence the incentive to save. Known as hard or sound money, such as those supported by a specie standard, high creation cost currencies maintain reliable mechanisms for restricting supply growth. In contrast, unsound money, or money that is easily prone to supply increases such as most government-issued money, is susceptible to rapid stock increases and wealth depreciation of current holders. The printing of unsound money has often been used to finance national spending, effectively pulling forward the future wealth of its citizens to fund the perceived needs of today. Evidence from the largest civilizations in history shows that sound money is necessary for progress and growth, and the lack of a stable monetary standard is generally associated with societal and economic destruction, such as with the collapse of the Roman Empire through its currency debasement. Digitally sound currencies such as Bitcoin may offer a solution to the historical and current problems of unsound money. At the same time, the authors must caution against the practical adoption of non-sovereign sound money, as the rapid adoption case for these new alternatives run diametrically opposed to the interests of the world’s largest sovereigns and central banking institutions who control their currency supply. However, we cannot ignore the fact that history has proven time and time again that once “sound” monetary media departs from this path via debasement, they will eventually be completely replaced by newer forms of more sound money.

Unsound Money

Government-issued money, like primitive money and most commodity-based monetary bases, is susceptible to rapid supply increases compared to its existing stock, and therefore has the potential (at all times) to lead to a rapid loss of salability, diminishment of purchasing power, and wealth depreciation of its current holders. With the suspension of the gold standard during early 1900s wartime, governments expanded money beyond their limited gold-back treasuries, spreading the liability of future repayment out to the entire population. Money (i.e., value and, more specifically, future value) was created in order to finance wartime needs, pulling forward the future wealth of its citizens. World War I may have ended far sooner had European nations remained on the gold standard and not been able to continue their war efforts with limited treasuries through the expansion of fiat money. In a sound monetary regime, a government’s wartime expenditures are bound by the taxes it can collect and savings it has amassed over time (in the form of hard money treasury), but with an unsound monetary regime, the only constraint is how much currency a government can create before each incrementally-created unit becomes exponentially less valuable (asymptotically approaches zero). In a fiat currency regime, value can appear simply through the creation of additional money, but only for so long as the population believes this new fiat value to be temporal (whether through the future creation of actual wealth or the future promise of a currency supply contraction). The Great Depression forced nations off the gold standard, while government control and socialization of the economy under Hoover and FDR continued to exacerbate the growth of unsound money, including Executive Order 6102 signed by FDR in 1933 which forbade the ownership of gold coin, bullion, and certificates and essentially allowed the federal government to confiscate its citizens’ wealth.

Hyperinflation is an economic phenomenon unique to rapidly inflatable commodity and government-controlled money. Given that the cost of production of government-issued money is effectively zero, there remains an ever-present temptation to create currency in order to satisfy short-term consumption demand, leading to a vicious, difficult-to-reverse cycle of borrowing from the future in order to satisfy the needs of the present. Through this, it is quite possible for the wealth of a nation to disappear in a relatively short time span through hyperinflationary government activity. Hyperinflation extends beyond simply the extreme loss of a nation’s wealth; it represents a complete collapse of the economic structure, production capability, and productivity of a society. The increasing monetary supply means a continuous devaluation of the currency, expropriating value from individuals who currently own wealth (and who have amassed it over the years and generations through sound saving behavior) to those who are first to receive the new money. This transfer of wealth from savers to “new money” is known as the Cantillon Effect: inflationary policy creates wealth for a government at the expense of current savers and holders, and the immediate beneficiaries are those who receive it once the government spends it. (1) The present and future wealth of citizens is reduced via inflationary policy, and so the income and wealth of a government is naturally reduced in the future with a decreased value of real tax receipts. In essence, inflationary policy eliminates the temporal element of future government income and wealth derived from citizen taxation by printing money and receiving it today. Whether the Cantillon Effect is a result of general inflationary policy or national emergencies that justify increased government spending to stabilize a languishing economy, the expansion of government money reduces the wealth of its current holders, decreases the incentive to save, and creates far more serious issues longer term if not managed by an ever-vigilant sovereign with an eye towards restoring the soundness of its money as quickly as possible. And, given the lack of tangible examples historically of a successful “return to sound money,” we grow increasingly concerned that, once down the path of openly borrowing from the future to pay for the present, modern societies may be practically incapable of breaking this cycle without a significant, adverse intervention.

Sound money makes societal efforts such as production, mutual cooperation, wealth accumulation, capital savings, and trade the only avenue open for fundamental prosperity rather than the creation of wealth for some through the dilution of others. The 1900s marked the transition from sound money to unsound money, backed by a government decree that denied a free market choice of monetary media and forced government-issued fiat currency into the hands of its citizens. Sound money is a key requirement of individual freedom from authoritarianism and despotism, as the coercive state’s capability to create infinite money can give it undue influence over its citizens, an influence which by its very nature can be most easily abused and attract those with suboptimal agendas.

Savings & Time Preference

Sound money is a key prerequisite for individual time preference choices, a critical and commonly ignored element of personal decision making. Time preference refers to an individual’s preference for current consumption over future consumption. Those with higher time preference are substantially focused on their well-being in the present and immediate future, while others with lower time preference place more emphasis on their well-being in the future. But this concept extends far beyond just the basic preference of the individual to consume; the economist Hoppe explains that once time preference of the individual drops low enough across a broad enough base of the population to allow for the production of widespread capital goods, it initiates the “process of civilization.” Per the original publication, the process of civilization is “a positive feedback loop where time preferences perpetually decrease due to the accumulation of capital, the increase of the relative value of future goods, the further division of labor, and lengthening of life expectancies.” (2) The consequences of the converse, a situation in which time preferences increase enough across a broad enough base of the population, should be obvious.

Microeconomics focus on individual decisions, and the most important economic decisions any individual can make are the tradeoffs they make today with their future self. The better money can retain its value through time, the more individuals (all else being equal) are incentivized to postpone present consumption and instead dedicate capital and resources for future production, leading to higher capital accumulation and improved quality of life. In instances where money does not retain its value through time, individuals are incentivized to consume rather than save and commit capital for the future, eventually leading to suboptimal capital allocation decisions and lower aggregate wealth levels. Unsound monetary standards have profound effects on societies in the long run: society in aggregate saves less, accumulates fewer resources, and consumes its capital at a faster pace. What’s worse is that this occurs in an almost paradoxical fashion, as individuals only “see” the short-term effects of an increased ability to consume, while continuing to fuel the long-term wealth decline of the society.

Societies and economic progress thrive under a sound monetary system; this progress disintegrates when monetary systems are debased. The Roman Empire, in part, collapsed due to the debasement of the Roman silver currency, the denarius. Trade was vital to Rome and generated the vast majority of the wealth of Roman citizens, allowing the capital to pay for the administration, logistics, military, and control of its 130 million people over 1.5 million square miles. In order to finance present spending, the denarius, originally comprised of 4.5 grams of pure silver, was debased by reducing the coin’s silver content from 90% to 50% (the economic equivalent of printing additional fiat currency today). Throughout the 2nd and 3rd century, the currency was continually inflated; eventually, the silver content was reduced to just 0.5%, the equivalent of having increased the supply of the denarius by 180x. The denarius currency debasement did not increase prosperity as it was initially intended; rather, it continually transferred saved wealth away from the people to the future dream of continued imperial expansion and made everyday commerce and labor increasingly challenged. With soaring logistical and administrative costs, particularly with financing the Roman Empire’s military efforts, Romans levied higher taxes on the citizens of the Empire, eventually leading to hyperinflation, a fractured economy, localization of trade, a financial crisis, and return to inefficient barter methods. Similar dynamics can be studied across the fall of the Byzantine empire and the modern-day struggles of European societies.

Unsound money controlled by central banks, whose express task is to keep inflation positive, adds potential real (and increasingly) adverse incentives for individuals to save. Only returns that are higher than the rate of inflation of the currency are positive in real terms, creating incentives for higher-return but higher-risk investment and accelerated spending. Savings rates on average have declined alarmingly across developed nations in the twentieth century, particularly after the suspension of the gold standard (Fig. 1). Meanwhile, household, municipal, and national debts have increased to considerably elevated levels. Sound money, on the other hand, has stable value and gains relative to other unsound money over time.

Fig. 1: US Personal Saving Rate, Seasonally Adjusted (3)

Keynesian high time preference thinking with abstained saving and urging of consumption as the key to economic prosperity has transformed capitalism, a system originally based on saving and capital accumulation, into a system of immediate gratification and consumption. Long term economic growth is unavoidably driven by delayed gratification, saving, and capital investment, thereby extending the production cycle and increasing the productivity of production. The transition from sound money to unsound money has led to wealth depreciation, a significant increase in consumption, and indebtedness as the commonplace method for funding such consumption.

Central Banking

In The Use of Knowledge in Society, Hayek argues that prices are information and a communication system of economic production among an economy that coordinates complex processes for production in a free market system. (4) A breakdown in the ability for prices to communicate information causes interruptions in economic activity, as the economy can no longer appropriately understand and measure resource scarcity and economic costs. Capitalist systems cannot properly function without a free market determination of the price of capital through the interaction of supply and demand, allocation of capital goods, and economic decisions driven by price signals. The adoption of the modern Keynesian capitalist structure (as opposed to traditional accumulation-based capitalism to which the authors remain fervent disciples), which has led to interest rate manipulation and monetary debasement, eliminates the incentive to accumulate capital and creates distortions in normal business cycles. Eventually, recessions and depressions result from future capital spending pulled forward in time, the mispriced cost of capital through interest rate manipulation, and lending capital to negative net present value endeavors.

Keynesians hold that business cycles are a result of flagging “animal spirits” and that central bankers and the government can engineer recoveries and growth through the printing of new money and higher government spending of the newly minted unsound money. However, economic logic shows that such actions simply attempt to paper over critical economic issues with a façade of control and hope that new economic activity will catch up in time. History shows us how the manipulation of money and the meddling of price discovery mechanism increase the severity of recessions, particularly under the erroneous notion that central banks can prevent or manage recessions. Central bank control of a money supply and interest rates distorts the signals and incentives for market participants to manage their consumption and production, eventually leading to a misallocation (sometimes to a severe degree) of capital and resources and potentially extensive failures and layoffs across industries. Sound money forces all market participants to be capital and resource efficient, and governments need to function in a fiscally responsible manner rather than with an endless supply of unsound money at their disposal. Without the presence of a central bank, individuals in a free market for money would choose reliable currencies with the highest stock-to-flow ratio that fluctuate the least with changes to the demand or supply of the currency. Such a concept is not fanciful or unprecedented; prior to the pervasion of Keynesian economics and the creation of floating exchange rates, individuals were able to create global business plans denominated in any currency without much regard for exchange rate fluctuations.

Data in Review

Central banks around the world have printed unprecedented quantities of money and, through their symbiotic and “independent” relationship with local governments, created substantial debt levels in the past century. Central banks and governments have in practice worked in concert to create and maintain business cycles through the issuance of debt by governments (fiscal policy) and subsequent open market purchases by central banks with self-created money (monetary policy). Having taken domestic money off the gold standard, central banks were free to print money, finance war efforts, and engineer business cycles. The wealth of the government was no longer limited by central bank gold reserves and its ability to tax its citizens; it could expand its wealth to that of all of its citizens and incur as much as debt as it wanted, because, as Nobel Prize laureate Krugman puts it, we owe it to ourselves. A government can continue to spend and pile up debt without ever having to worry about paying it off because the government can tap into a central bank’s money press. Data from the last century is quite alarming: global debt has skyrocketed amidst a continuous debasement of fiat money through printing.

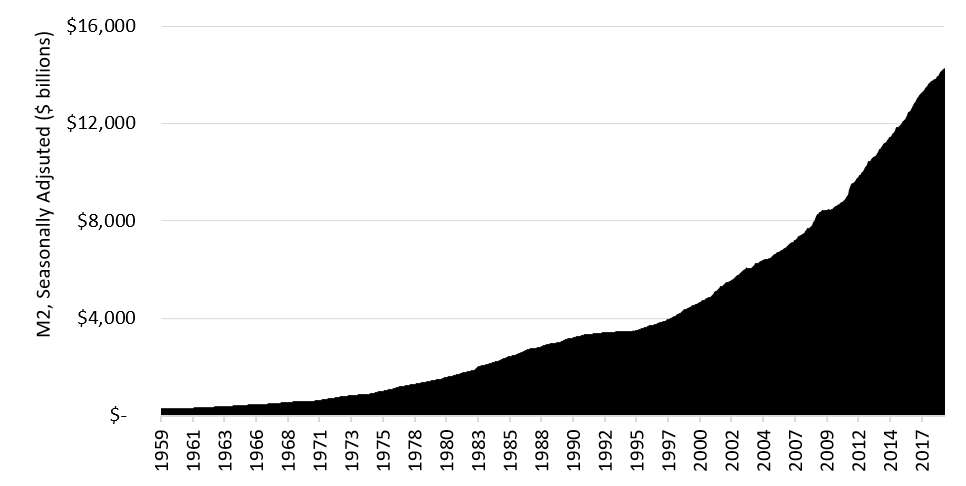

Fig. 2: United States Dollar - M2 Money Stock (5)

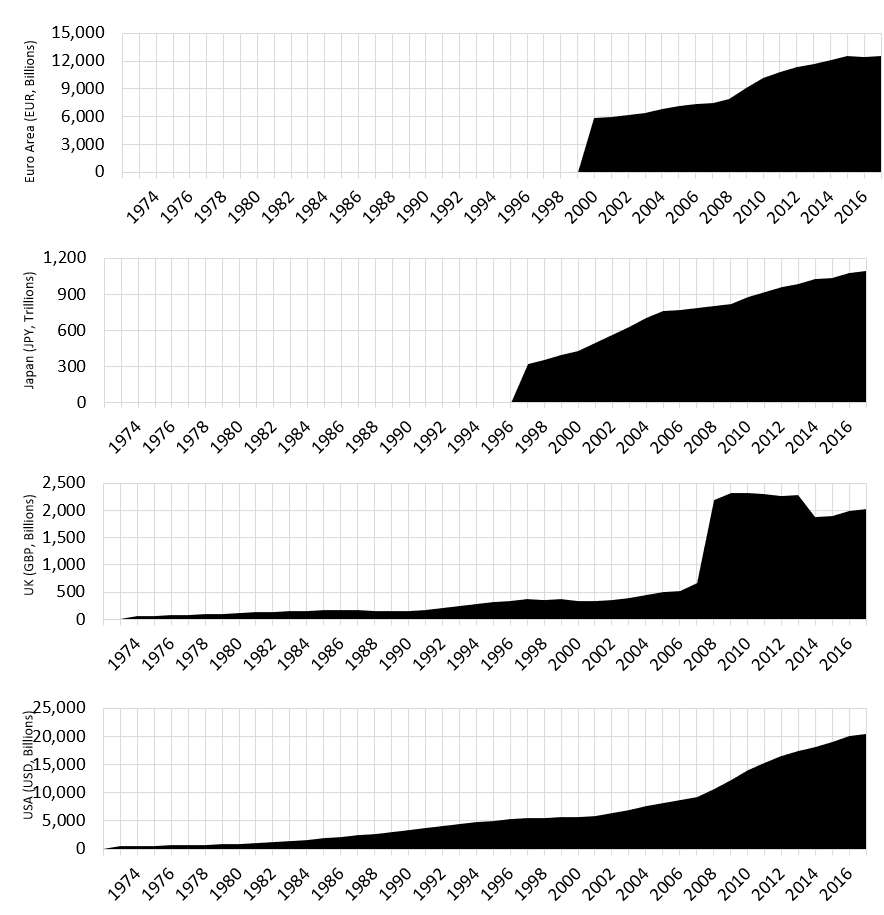

Fig. 3: Government Debt (6)

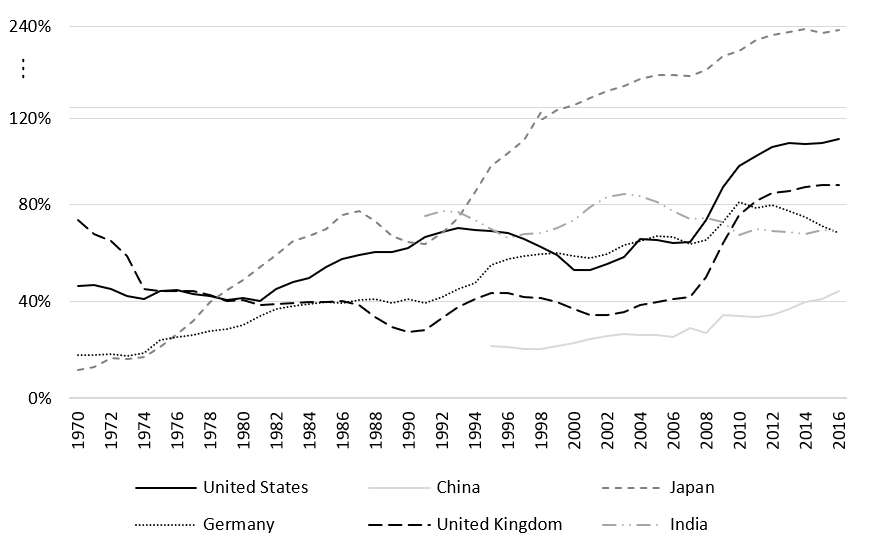

Fig. 4: General Government Debt (Percent of GDP). (7)

Since debt-to-GDP ratios are an indicator of an economy’s health and a key factor in government finance sustainability, rising debt-to-GDP ratios suggest untenable federal spending practices and inevitably either lead to currency collapses or long periods of federal austerity (depending, in part, whether its debt is denominated in local or foreign currency). The future spending that was brought forward in time through deficits and debt accumulation will unavoidably need to be paid back with periods of lower spending. Otherwise, governments will be unable to pay rising debt interest payments, need to continue to print money to cover the nominal cost of debt, and levy heavy taxes on its citizens, depressing economic growth, decreasing confidence in the currency, and creating a deeply inflationary (and perhaps even hyperinflationary) cycle. A government’s debt level and its sustainability, credibility of a government as a lender, money stock changes, the credibility of a currency, and the value of a currency are closely linked; if any fall out of sync with the others, it can create monetary and financial crises. In truth, it’s unknown what specifically tips the balance out of favor and when, though crashes of imperial powers of the past show us the severe consequences that result from lack of credibility of a government as a lender, uncontrolled money debasement, or fading confidence in a currency.

Sound Digital Money

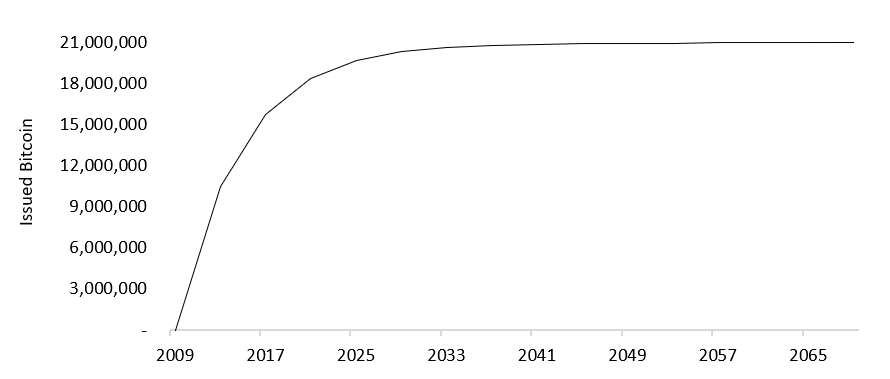

In the search for a digitally sound money, Bitcoin was the first digital payment system that did not rely on a trusted third-party intermediary. Bitcoin is verifiably digitally scarce with a known supply issuance in perpetuity: the total supply is limited to 21 million bitcoin and employs a variant of Milton Friedman’s k-percent rule where the annual money supply growth is fixed. (8) Supply issuance declines every 210,000 blocks (approximately every 4 years) as the block reward halves. At its introduction in 2009, bitcoin’s block reward was 50 bitcoin per block, and halved to 25 bitcoins in 2013 and 12.5 bitcoin in 2016. In contrast to modern central banking where newly issued money is used to finance government spending and lending, newly issued bitcoins are provided as compensation to individuals who expend resources to update the distributed ledger, and more importantly are “created” under a fixed, known, and unalterable issuance schedule (Figure 5).

Fig. 5: Bitcoin Supply Issuance (9)

The difficulty adjustment in Bitcoin, or the method that modulates supply creation with increased network resources, acts as a reliable method for limiting the stock-to-flow ratio increases and makes bitcoin fundamentally unique from all other forms of money. Growth in bitcoin’s value also cannot increase its supply, making it a durable hard money, as the supply of the network is naturally bounded by the hard-coded algorithm and the dynamically adjusted difficulty of the network. Furthermore, network security lies in the asymmetry of the costs of performing the “proof-of-work” necessary to validate transactions and the cost of verifying completeness and truthfulness: it is relatively difficult and expensive to performance the calculations in the first place but trivial to verify the computations are correct.

The presence of a conservative monetary policy and the difficulty adjustment allows bitcoin to theoretically succeed as a digital store of wealth and as a transferable monetary media. While many will point towards bitcoin’s volatility as an insurmountable hurdle for its adoption as a store of wealth or transactional currency, its volatility today, while still early in its global adoption, is a result of its programmable, inflexible supply and predetermined growth rate; demand changes of the underlying units do not affect the creation or destruction of the units. Therefore, as bitcoin adoption increases (and bitcoin market cap increases given its fixed, known supply), each incremental adopter will by definition have a decreasing impact on the price of bitcoin, leading to a dampening of volatility in the long run. So, while bitcoin’s volatility is natural and quite expected during its early stage of global adoption, this volatility should not be confused with its expected volatility at mature adoption, whereas its properties make it very much a fundamentally good store of value. Bitcoin is one of the very few assets that has strict limited scarcity and the only monetary media that is guaranteed to not be debased. In addition, bitcoin does not have any of the physical drawbacks of traditional money or stores of wealth: the cost and speed of transfer and general storage is a significant improvement over traditional media.

Bitcoin created an independent alternative mechanism for global payments that does not require a trusted 3rd party intermediary and can function entirely separately from the existing financial system. Bitcoin combines the finality of cash settlement with the benefits of digitization, creating a fast method for large payment settlement across borders. While it may compete with central banks and large financial institutions that perform international payment settlements, Bitcoin has a distributed, verifiable ledger, cryptographic security, is practically resistant to threats, and bears no counterparty risk or reliance on a trusted third-party. If bitcoin achieves a long-term stability in value, bitcoin could be a superior alternative to using unsound fiat money for global payments and storing wealth, one that is truly decentralized and exists in a balanced equilibrium of transaction processors, developers, and users. Even if it does not become a ubiquitously superior alternative to central banking, bitcoin at the very least provides an alternative sound money option that can be leveraged from time to time by any global citizen in need of reprieve from local currency inflation.

For an asset that exhibits annualized volatility in excess of 50%, one could argue that utilizing bitcoin for everyday economic transactions should be prohibitively challenging. However, it is imperative to consider a few key points. First, bitcoin’s high volatility is primarily a function of high marginal demand relative to its existing stock and market capitalization. High marginal buying and selling relative to a low market capitalization (c. $64bn as of February 2019) will naturally create outsized volatility. Should bitcoin’s market capitalization grow to accommodate its demand fluctuations, its volatility should decline as marginal buying and selling are smaller relative to the outstanding value of the asset. Second, bitcoin today represents a speculative, venture-like investment for many who own the asset. Accordingly, investors should have higher expected returns in order to compensate for the higher risk of the investment, and as a result should naturally expect higher volatility. Volatility should naturally decline as the ownership of the outstanding stock changes from speculative to more stable investors. Finally, bitcoin’s volatility is generally measured versus a fiat currency, primarily the US dollar. However, the value of sound money is not its value relative to other currencies, but rather its purchasing power versus a basket of goods and services. Bitcoin is designed to be a “stablecoin” against purchasing power, and therefore its volatility should be measured against its ability to purchase goods and services. (10) The vast majority of global economies experience positive inflation and have for the past century following the suspension of the gold standard. Positive inflation indicates that the value of an underlying basket of goods and services has appreciated versus the fiat currency it is tied to; conversely, it means that each unit of currency has reduced purchasing power and is marginally worse at its primary function (to pay for goods, services, and labor). Hence, the volatility of bitcoin, like other forms of money, should be measured against its purchasing power in local economies as opposed to other fiat currencies to account for real and not nominal volatility.

We highlight two seemingly opposite examples of purchasing power lost by unsound fiat currency to illustrate this phenomenon: the Venezuelan bolivar and the US dollar. In the first example, hyperinflationary policies in the late 2010s have led to a massive depreciation of the bolivar, eradication of individual wealth, and extreme poverty for a vast majority of its citizens. At the end of 2018, Venezuela’s inflation rate topped 80,000% (2018-end estimates for Venezuela’s inflation rate have wildly varied from 80,000% all the way to 1,000,000%), essentially meaning that each unit of local currency has effectively lost 100% of its purchasing power. Daily inflation is roughly 220%, or in other words every $100 is worth just $31 a mere 24 hours later. This massive loss of purchasing power has taken place over a relatively short time frame, but such dynamics can also be observed in the United States dollar throughout the past century: from 1913 to 2018, the value of the US dollar has fallen over 96%. Figure 6 depicts the loss of purchasing power of $100 US dollars since 1913. Over just the last ten years, the US dollar has lost 16% of its purchasing power ($4.70 to $3.90 on Fig. 6’s scale). Though the loss of the US dollar’s purchasing power is more drawn out and less extreme than that of the Venezuelan bolivar, the stark and sobering conclusion is the same: fiat currencies have unarguably failed to maintain their purchasing power, perhaps money’s only core requirement and reason for existence. Despite its volatility and multiple bull-bear cycles, bitcoin has unequivocally increased its purchasing power, rising from $0 to $3500, in the ten years since its creation.

Fig. 6: Purchasing power of the US dollar, monthly. (11)

Other digital assets that exhibit characteristics of sound money with high stock-to-flow ratios, sufficient network and cryptographic attack resistance, and inflation protection could also serve as sound monies. In part, the objective elements of a money must also be considered with its degree of social acceptance: money has value because society demands the benefit it offers in purchasing power for labor, goods, and services. Because society is willing to accept and give money as forms of payment, its value in part is derived from its social convention. It is entirely possible that bitcoin may be disrupted and lose market share to a future sound money. Sound monies with equivalent objective and social characteristics theoretically share the market for sound money, all else being equal, though in practice, network effects, feature sets, first mover advantages, and social convention create unequal growth rates and market shares. In this light, the search for digitally sound money does not end with bitcoin; it has actually begun with bitcoin and now has opened up the possibility for a more free and accessible market for sound money for the global citizen.

Acknowledgements

The authors would like to acknowledge Saifedean Ammous, PhD, author of The Bitcoin Standard, and Ray Dalio, founder of Bridgewater Associates and author of Principles for Navigating Big Debt Crises, for their influence on this essay. Ammous’ book provided the initial inspiration for the authors to delve into the history, dynamics, and evolution of monetary systems; many of his views that the authors share present themselves in this work. Dalio’s multi-decade study on understanding the engine of economic and financial systems, its cause-effect relationships, and models for navigating debt crises remain closely-held guiding principles for the authors.

Citations

(1) Cantillon, R. (1755). An Essay on Economic Theory (Essai sur la Nature du Commerce en Général. https://doi.org/10.1215/00182702-1811397

(2) Hoppe, H.-H. (2001). Democracy, The God That Failed: The Economics and Politics of Monarchy, Democracy, and Natural Order. Transaction Publishers. https://doi.org/10.1111/1467-8365.12281

(3) Federal Reserve Bank of St. Louis. (2019). US Personal Saving Rate, Percent, Monthly, Seasonally Adjusted Annual Rate.

(4) Hayek, F. (1945). The Use of Knowledge in Society. The American Economic Review. https://doi.org/10.1017/CBO9780511817410.007

(5) Federal Reserve Bank of St. Louis. (2018). M2 Money Stock, Billions of Dollars, Monthly, Seasonally Adjusted.

(6) Bloomberg L.P. (2018). Government Debt Data. Bloomberg L.P.

(7) OECD. (2018). General government debt. Retrieved from https://data.oecd.org/gga/general-government-debt.htm

(8) Bitcoin with an uppercase B refers to the network, bitcoin with a lowercase b refers to the monetary unit in the network.

(9) Blockchain Luxembourg S.A. (2018). Bitcoins in circulation. Retrieved from https://www.blockchain.com/charts/total-bitcoins

(10) Stablecoins are digital assets designed to maintain stable value against a real-world asset or basket through pegged collateralization or algorithmic adjustments. The most common stablecoins include digital representations of fiat currencies such as US dollars through collateralized deposits at a bank.

(11) Federal Reserve Bank of St. Louis. (2019). Consumer Price Index for All Urban Consumers: Purchasing Power of the Consumer Dollar, Index 1913=100, Monthly, Not Seasonally Adjusted.

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsementof any of the digital assets or companies mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2019. All rights reserved.